Ninety-two percent of global banks now report active AI deployment in at least one core banking function. Yet most institutions are still only scratching the surface of what AI agents — not just AI tools, not just chatbots — can actually do across their operations.

The distinction matters. AI agents don't just answer questions or generate summaries. They perceive context, make decisions, execute multi-step workflows, and loop back to verify outcomes — all with minimal human intervention. In banking, where regulatory oversight is constant, exceptions are the norm, and the cost of slow decisions compounds daily, that difference is the difference between incremental efficiency and genuine transformation.

This guide covers 25+ real AI agent use cases in banking across compliance, customer operations, core banking, analytics, and fintech — with outcomes drawn from live deployments, not theoretical models. Whether you're at a global bank, a regional credit union, or a growing fintech, this is where you'll find the use cases most relevant to where your organisation is right now.

What you'll find in this guide:

- A clear definition of what an AI agent actually is (and how it differs from what you've tried before)

- 25+ specific use cases in banking, grouped by operational domain

- Real deployment outcomes from financial services institutions

- A practical framework for choosing where to start

- Answers to the questions your leadership team is probably already asking

What is an AI agent in banking?

An AI agent in banking is an autonomous software system that perceives context, makes decisions, and executes multi-step workflows — from fraud screening to dispute resolution — across connected banking systems with minimal human input. Unlike a chatbot that responds to queries or an RPA bot that follows rigid rules, an AI agent plans, reasons, handles exceptions, and adapts as conditions change.

Why AI Agents — Not Just AI Tools — Are What Banking Actually Needs

For years, banks invested in two categories of automation: chatbots for customer-facing queries, and robotic process automation (RPA) for structured back-office tasks. Both delivered value. Both also hit hard limits.

Chatbots fail the moment a conversation goes off-script. RPA breaks the moment a document format changes or a workflow requires a judgment call. And neither can handle the reality of modern banking operations: fragmented systems, regulatory complexity, exception-heavy workflows, and decisions that need to be made in real time, at scale, with a full audit trail.

AI agents change that equation. Where a chatbot responds, an agent acts. Where RPA follows rules, an agent reasons. Where traditional automation stalls on exceptions, an agent escalates, adapts, or routes — within governed guardrails your compliance team can actually stand behind.

The numbers reflect this shift. According to McKinsey, early agentic AI deployments are reducing manual workloads by 30–50% in financial services operations. Fraud losses globally now exceed $190 billion annually, with compliance teams spending as much as 42% of their budgets on false positives and manual reviews — both problems AI agents are specifically built to address. In 2025 alone, fifty of the world's largest banks announced more than 160 agentic AI use cases.

The question is no longer whether AI agents work in banking. It's which use cases to prioritise, and how to get to production without a 12-month implementation cycle.

25+ AI Agent Use Cases in Banking

Category A: Compliance and Risk

Compliance is where the cost of getting things wrong is highest — and where AI agents deliver some of their most measurable outcomes. The following use cases address the workflows that consume the most manual effort and carry the most regulatory exposure.

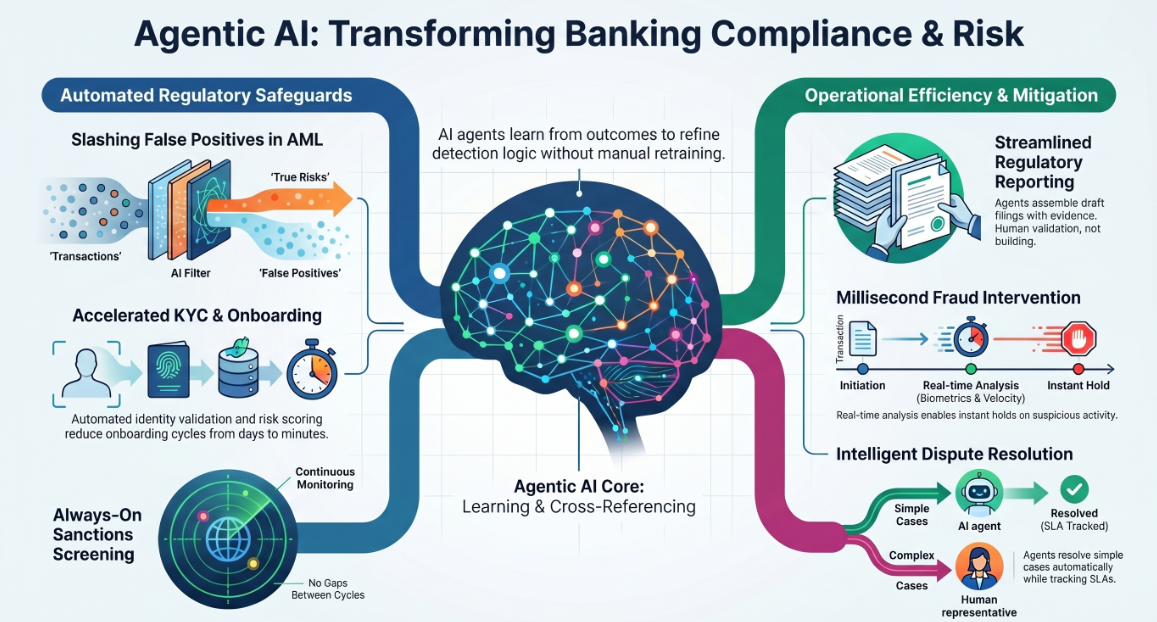

1. AML Transaction Monitoring

AI agents continuously monitor transaction flows, applying behavioural analytics and pattern recognition to flag anomalies in real time. Unlike static rule-based systems that generate high false positive rates, agentic systems learn from case outcomes and refine their detection logic without manual retraining. Agents can cross-reference multiple data sources simultaneously — transaction history, customer profiles, geographic risk signals, and external databases — and generate alert packages with full evidence chains ready for investigator review.

Deployment outcome: Significantly reduced false positive volume, faster alert triage, and audit-ready investigation documentation generated automatically.

2. KYC and Customer Due Diligence Automation

Customer onboarding in banking involves identity verification, document validation, beneficial ownership checks, PEP screening, and risk scoring — a sequence that traditionally takes days and involves multiple teams. AI agents handle the full KYC lifecycle: ingesting identity documents, validating authenticity, running sanctions and adverse media checks, assigning risk tiers, and flagging cases requiring enhanced due diligence (EDD) for human review. Every step is logged with timestamps and evidence, creating a defensible audit trail.

Deployment outcome: Reduced onboarding cycle time, lower drop-off rates, and consistent risk classification across all customer segments.

3. Sanctions and PEP Screening

AI agents run continuous screening against sanctions lists, politically exposed person (PEP) databases, and adverse media sources — not just at onboarding, but on an ongoing basis as customer profiles and risk environments evolve. Agents flag changes, generate risk update summaries, and route cases to compliance teams with context already assembled. This eliminates the periodic batch-screening model that leaves gaps between review cycles.

Deployment outcome: Always-on monitoring replacing periodic manual checks, with faster escalation and fewer missed updates.

4. Regulatory Reporting Automation

Generating SARs, CTRs, FBARs, and jurisdiction-specific regulatory filings is one of the most resource-intensive tasks in bank compliance. AI agents automate the assembly of these reports by pulling structured data from across core banking, case management, and transaction monitoring systems, applying regulatory templates, and producing draft filings with supporting evidence. Human reviewers validate and submit rather than build from scratch.

Deployment outcome: Faster reporting cycles, reduced analyst time on routine filing preparation, and improved accuracy through automated cross-referencing.

5. Fraud Detection and Real-Time Risk Scoring

AI agents analyse transactions the moment they occur, scoring risk across multiple dimensions — device fingerprinting, behavioural biometrics, transaction velocity, geographic anomalies, and network relationships. When a transaction crosses a risk threshold, the agent can trigger a hold, request step-up authentication, initiate an investigation workflow, or notify the customer — all within milliseconds. Over time, agents refine their models based on confirmed fraud outcomes, improving precision continuously.

Deployment outcome: Real-time fraud intervention, significant reduction in false positives, and lower financial losses through earlier interception.

6. Disputes and Chargeback Workflow Automation

Dispute resolution is one of the most labour-intensive workflows in retail banking. AI agents triage incoming disputes by type and complexity, retrieve relevant transaction records and communications, apply resolution logic based on card scheme rules and internal policy, and either resolve straightforward cases automatically or prepare case summaries for human reviewers. SLA tracking runs continuously, with automated escalation when timelines are at risk.

Deployment outcome: Faster dispute resolution, reduced operational load on dispute teams, and improved SLA adherence through automated routing and tracking.

Category B: Customer Operations

Customer-facing operations in banking are increasingly high-volume, multi-channel, and expectation-heavy. AI agents handle the complexity without the headcount.

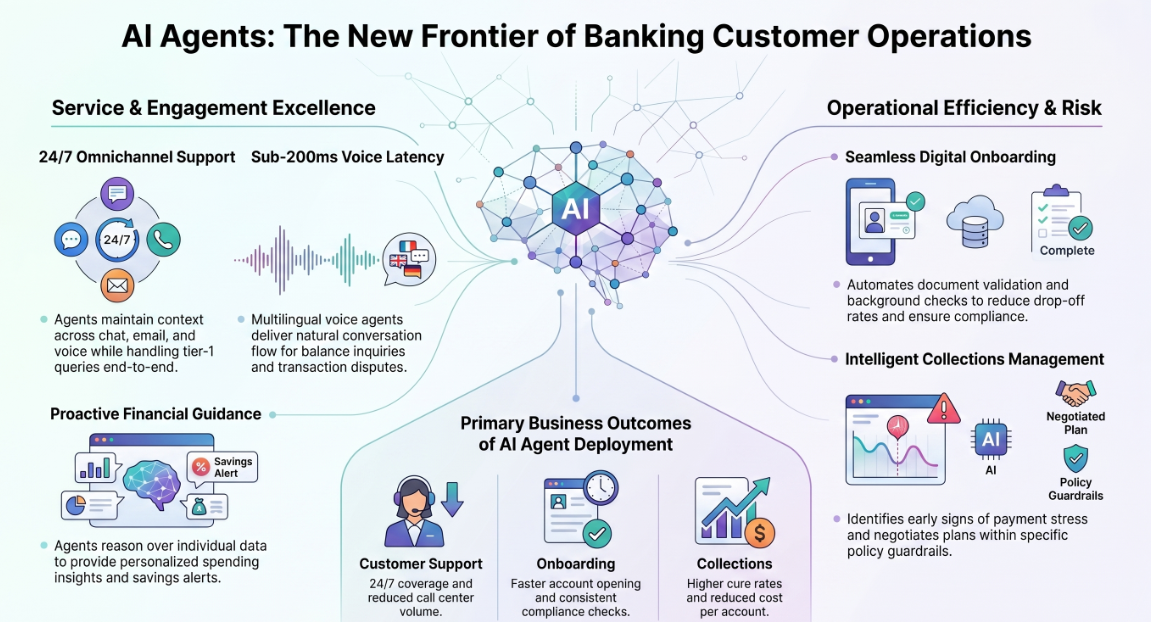

7. Omnichannel Customer Support

AI agents manage customer enquiries across chat, email, voice, and messaging platforms like WhatsApp — maintaining context across channels and routing intelligently to the right team or resolution path. Unlike scripted bots, these agents understand intent, retrieve account-level context from core banking systems, and handle tier-1 queries end to end. When escalation is needed, they hand off with a full conversation summary so the human agent never starts from zero.

One live deployment in financial services covered omnichannel intake across chat, email, and phone, with agent-assist summarisation, next-best-action recommendations, and full SLA monitoring baked into the workflow. Outcomes included reduced manual helpdesk burden, faster case handling, and measurably improved compliance readiness through automated audit trails.

Deployment outcome: 24/7 customer coverage, reduced call centre volume, and consistent service quality across channels.

8. Voice Banking Agent (Multilingual)

AI voice agents handle inbound customer calls using speech-to-text, large language model reasoning, and text-to-speech pipelines — delivering sub-200ms response latency and natural conversation flow. They handle balance enquiries, transaction disputes, card activations, branch routing, and account servicing in multiple languages. When calls require human involvement, the agent transfers with a live transcript and context summary.

Deployment outcome: Reduction in IVR abandonment, faster call resolution, and expanded language coverage without additional staffing.

9. Customer Onboarding and Account Opening

AI agents guide new customers through the onboarding journey — collecting information, validating documents, running background checks, and provisioning accounts — without manual handoffs between teams. The agent manages the entire sequence, flags exceptions, and provides real-time status updates to the customer throughout.

Deployment outcome: Faster onboarding completion, lower drop-off rates, and consistent compliance checks on every application.

10. Personalised Financial Guidance

AI agents connected to customer financial data can deliver personalised insights — spending pattern summaries, savings opportunity alerts, cashflow projections — through mobile banking interfaces or messaging channels. This goes beyond generic content: the agent reasons over the individual customer's data and generates specific, actionable guidance in plain language.

Deployment outcome: Increased engagement, improved financial outcomes for customers, and reduced inbound support volume through proactive communication.

11. Collections and Delinquency Management

AI agents monitor account health, identify early signs of payment stress, and trigger appropriate outreach through the right channel at the right time. They personalise communication tone and content based on customer profile and delinquency stage, and can negotiate payment plans within policy guardrails — escalating to human agents only when the situation requires judgement beyond the agent's scope.

Deployment outcome: Earlier intervention, higher cure rates at lower delinquency stages, and reduced collections cost per account.

Category C: Core Banking Operations

Back-office and operational workflows carry a disproportionate share of manual work in most banks. AI agents address the highest-friction points across the operational stack.

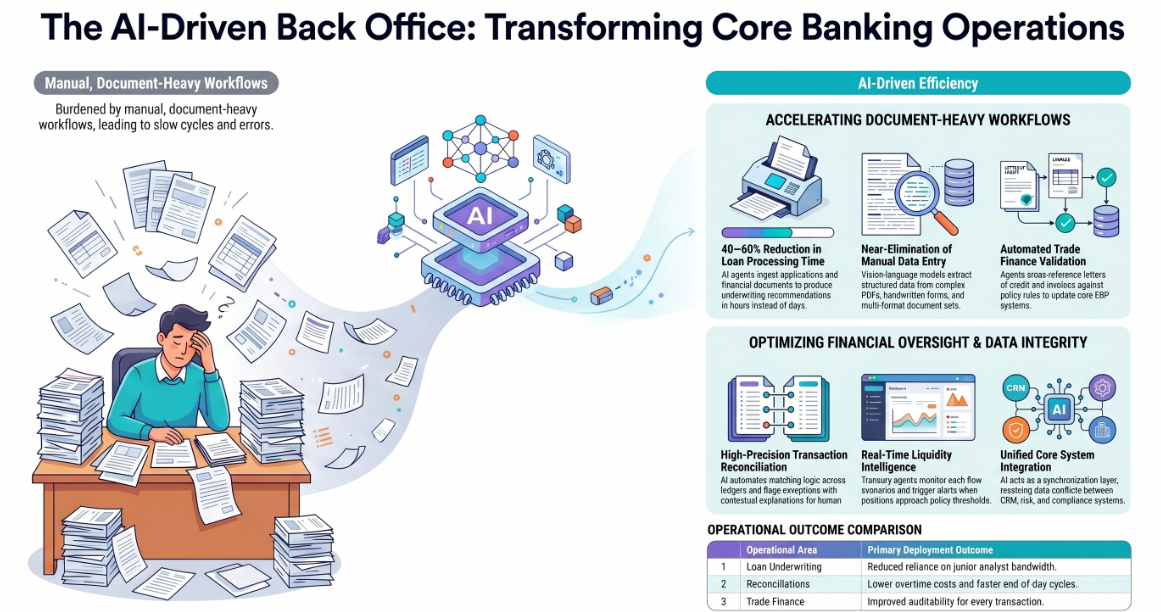

12. Loan Underwriting and Credit Decisioning

Loan processing is traditionally one of the most document-heavy, delay-prone workflows in banking. AI agents ingest loan applications, extract and validate data from financial documents, run credit models, check policy eligibility, and produce underwriting recommendations — reducing the process from days to hours. For straightforward applications, the agent produces a decision with supporting rationale. For complex cases, it assembles the package for human review.

Deployment outcome: 40–60% reduction in processing time (consistent with industry benchmarks), improved decision consistency, and reduced reliance on junior analyst bandwidth.

13. Document Processing and Data Extraction

Banking generates enormous volumes of unstructured documents — loan files, trade confirmations, KYC packs, contracts, regulatory filings. AI agents use vision-language models to extract structured data from these documents at scale, validate it against source systems, and route it into the appropriate workflows. Complex PDFs, handwritten forms, and multi-format document sets are all in scope.

Deployment outcome: Near-elimination of manual data entry, faster document processing cycles, and significantly reduced extraction error rates.

14. Reconciliations and Back-Office Automation

Reconciling transactions across systems, ledgers, and counterparties is time-consuming, error-prone, and low-value when done manually. AI agents automate the matching logic, flag unmatched items with contextual explanations, and route exceptions for human resolution. Audit logs are maintained throughout, providing a complete record of every reconciliation action.

Deployment outcome: Faster end-of-day reconciliation cycles, lower error rates, and reduced overtime cost on manual reconciliation tasks.

15. Trade Finance and Sales Order Workflow Automation

Processing trade finance documents — letters of credit, bills of lading, invoices — requires cross-referencing multiple documents against policy rules and system records. AI agents automate this document ingestion and validation, create or update records in core systems (including ERP platforms like SAP), and flag exceptions for human review. Rules-based governance handles approvals and escalations.

One live deployment replaced a legacy document processing environment facing end-of-life, automating the interpretation of order triggers, validation, and SAP sales order creation — with full audit logs and reconciliation reporting built in. Outcomes included faster order-to-confirm cycles, fewer data entry errors, and reduced dependency on legacy licensing costs.

Deployment outcome: Faster trade processing, reduced manual document handling, and improved auditability for every transaction.

16. Treasury and Liquidity Management

AI agents monitor liquidity positions in real time, model cash flow scenarios under different conditions, and generate alerts when positions approach policy thresholds. They can pull data from multiple treasury management systems, apply forecasting models, and surface recommendations for funding decisions — giving treasury teams decision-ready intelligence rather than raw data.

Deployment outcome: Earlier detection of liquidity risks, faster decision cycles, and improved confidence in treasury position accuracy.

17. Core Banking System Integration and Data Sync

Fragmented data across core banking, CRM, risk, and compliance systems creates blind spots and delays. AI agents act as intelligent integration layers, maintaining synchronised views of customer, account, and transaction data across systems — resolving conflicts, flagging data quality issues, and ensuring that every downstream workflow is operating on accurate, current information.

Deployment outcome: Reduced integration maintenance burden, improved data quality across systems, and faster downstream workflow execution.

Category D: Analytics and Intelligence

The gap between data that exists in banking systems and insight that reaches decision-makers is one of the most persistent and costly problems in the industry. AI agents close it.

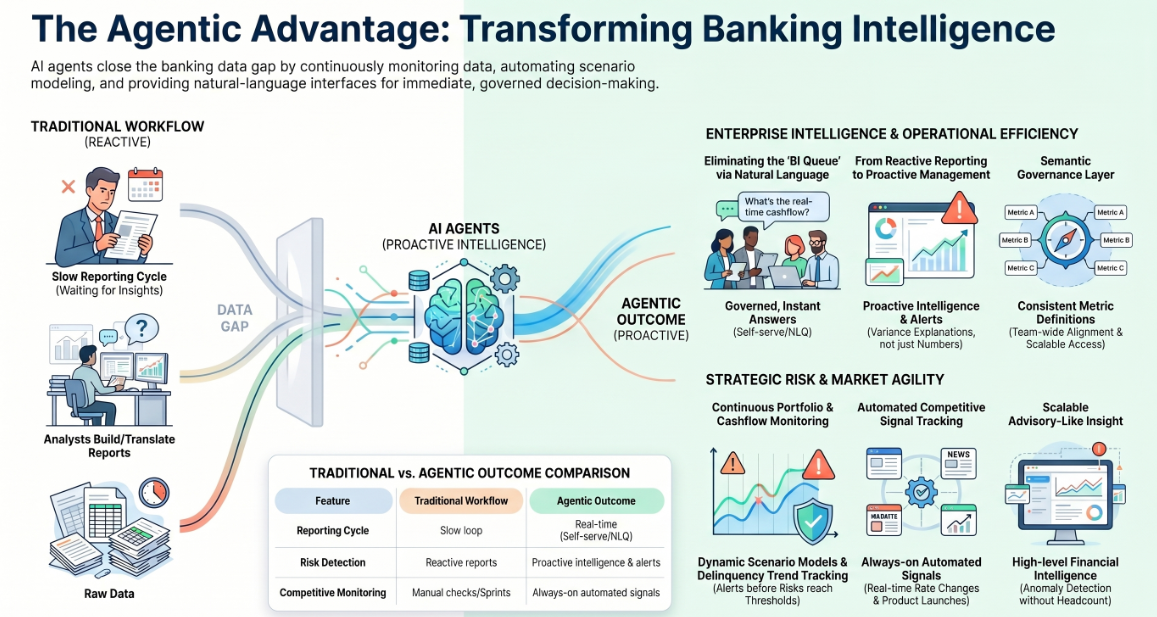

18. Agentic Business Intelligence

Traditional BI requires analysts to build reports, run queries, and translate data into narratives — a slow loop that delays decision-making and creates bottlenecks. Agentic BI platforms let leadership and operations teams query live data in natural language, receive governed answers with consistent metric definitions, and surface anomalies automatically — without waiting for the BI queue.

One live deployment in financial services delivered an NLQ interface over live operational data, a semantic governance layer for consistent definitions, and automated insight generation. Outcomes included faster strategic visibility without BI queueing, improved team-wide alignment through consistent metrics, and scalable insight access across functions.

Deployment outcome: Self-serve analytics for non-technical users, faster decision cycles, and reduced analyst dependency on routine reporting requests.

19. Portfolio Risk Analytics and Exception Alerting

AI agents monitor portfolio health continuously — tracking delinquency trends, concentration risk, maturity profiles, and residual value exposures — and generate alerts when metrics breach thresholds or move in patterns that warrant attention. Portfolio managers receive proactive intelligence rather than reactive reports.

Deployment outcome: Earlier identification of portfolio risks, faster leadership response to emerging issues, and improved decision support for portfolio management teams.

20. Cashflow Forecasting and Scenario Modelling

AI agents connect to accounting systems, banking feeds, and operational data to build dynamic cashflow models. They run scenarios, project runway under different conditions, and alert treasury or finance leadership when risks approach critical thresholds. For growing businesses and financial platforms serving CFOs, this replaces manual spreadsheet modelling with continuously updated, agent-generated intelligence.

One live deployment for a financial platform serving CFOs and advisors built a financial data connection layer, forecast and scenario modelling agents, and cash risk alerting — delivering faster analysis cycles, earlier detection of anomalies, and scalable advisory-like insight without additional headcount.

Deployment outcome: Continuous cashflow visibility, earlier cash risk detection, and faster financial decision-making for leadership.

21. Competitive Intelligence and Market Signal Monitoring

For banks operating in price-sensitive markets, keeping pace with competitor moves — rate changes, product launches, promotional activity — is a continuous intelligence challenge. AI agents monitor competitor channels, aggregate signals, and deliver structured intelligence to product and pricing teams through automated alerts and dashboards.

Deployment outcome: Always-on competitive monitoring replacing manual checks, faster competitive response cycles, and earlier identification of pricing gaps.

22. Operational KPI Monitoring and Variance Alerts

AI agents track operational metrics across departments — processing volumes, SLA adherence, error rates, cost per transaction — and generate variance alerts when performance deviates from targets. Leadership receives insight packs with explanations, not just numbers, enabling faster diagnosis and response.

Deployment outcome: Shift from reactive reporting to proactive operational management, with standardised metrics and automated task creation for exception resolution.

Category E: Fintech and Enterprise-Specific Use Cases

The following use cases are particularly relevant for fintechs, financial platforms, and enterprises with banking-adjacent operations.

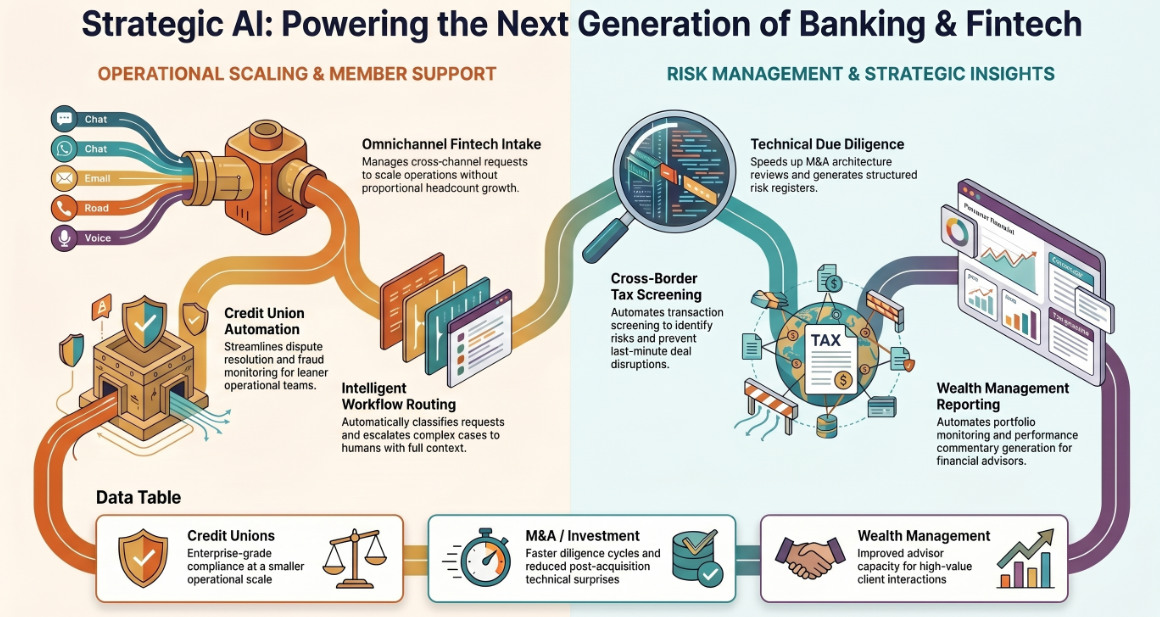

23. AI for Credit Unions: Disputes, Fraud, and Compliance Automation

Credit unions face the same compliance and operational demands as larger banks but with leaner teams. AI agents built for credit unions handle omnichannel member support, dispute intake and resolution, fraud monitoring, and regulatory workflow automation — at a scale and cost profile appropriate for the sector. Auditability and human-oversight controls are built in from the start.

One live deployment for a global fintech provider serving banks and credit unions delivered omnichannel intake, workflow routing, agent-assist next-best actions, and full audit trails. Outcomes included faster case handling, reduced operational load, and improved compliance readiness.

Deployment outcome: Enterprise-grade compliance capabilities at credit union operational scale, with measurably reduced manual workload.

24. AI for Fintech Operations: Omnichannel Intake and Workflow Routing

Fintechs operating at scale need to handle customer and operational workflows across multiple channels without building large support organisations. AI agents manage intake across chat, email, and messaging, classify and route requests intelligently, handle straightforward cases autonomously, and escalate complex cases with full context to human teams.

Deployment outcome: Scalable operations without proportional headcount growth, faster response times, and improved customer experience consistency.

25. Technical Due Diligence for Banking Investment and M&A

When banks, holding companies, or investors evaluate acquisitions in the financial technology sector, the technical diligence process is often slow, inconsistent, and reliant on scarce specialist capacity. AI agents accelerate this by conducting architecture reviews, assessing scalability and security posture, evaluating integration readiness, and generating structured risk registers with remediation roadmaps.

One live deployment for a holding company evaluating a mobile banking acquisition delivered code and architecture review, infrastructure and security assessment, scalability and resilience analysis, and a full risk register with prioritised remediation steps. Outcomes included faster investment decisions, reduced post-deal surprises, and greater confidence in scalability and security posture.

Deployment outcome: Faster diligence cycles, structured risk visibility, and reduced post-acquisition technical surprises.

26. Tax and Cross-Border Transaction Risk Screening

Banks and financial institutions processing cross-border transactions face withholding tax, VAT, and permanent establishment risks that are complex to screen manually at transaction speed. AI agents automate pre-screening of transactions, classify risk types, assemble evidence, generate explainability notes for compliance records, and route flagged cases to tax specialists with supporting context already prepared.

Deployment outcome: Earlier detection of cross-border tax risks, reduced last-minute deal disruptions, and faster pre-compliance review cycles.

27. Financial Advisor Support and Portfolio Reporting Automation

Wealth management and advisory operations require continuous portfolio monitoring, client reporting, and performance commentary generation — all highly manual today. AI agents consolidate portfolio data across entities, generate client-ready reports with narrative commentary, monitor for performance anomalies, and alert advisors when client situations require proactive outreach.

Deployment outcome: Faster client reporting cycles, scalable advisory insight generation, and improved advisor capacity for high-value client interactions.

What Real Deployments Actually Look Like

Understanding use cases in the abstract is useful. Seeing what they look like in practice is more useful.

Across live deployments in the financial services sector, several patterns emerge consistently:

Pattern 1: Compliance workflows go from days to hours. In KYC and AML implementations, the combination of document extraction, database cross-referencing, and automated case assembly compresses what previously took analyst teams days into a workflow that completes in hours — with higher consistency and a complete audit trail as a by-product.

Pattern 2: Omnichannel support scales without linear headcount growth. Financial services operators that deploy omnichannel AI agents consistently report that they handle significantly higher query volumes without proportional increases in support headcount. The agent manages tier-1 and many tier-2 queries autonomously, with human agents handling only the cases that genuinely require judgement.

Pattern 3: Agentic BI eliminates the reporting bottleneck. When business teams can query live data in natural language and receive governed, explainable answers, the BI queue collapses. Leadership teams get faster access to the information they need, and data teams spend less time on routine report requests and more on complex analytical work.

Pattern 4: Cashflow and portfolio intelligence becomes proactive. Organisations that deploy forecasting and monitoring agents report a consistent shift from reactive reporting — where leadership learns about a problem after it has escalated — to proactive management, where the agent surfaces risks while they are still addressable. Earlier detection of cash risks and anomalies is the most commonly cited outcome.

Pattern 5: Governance is built in, not bolted on. The most successful banking deployments treat audit trails, human oversight, and escalation logic as foundational design requirements — not afterthoughts. Every agent action is logged, every exception is routable, and every output is explainable. This is what makes AI agents viable in regulated environments.

How to Choose Where to Start

Not every use case is equally ready to deploy, and not every bank has the same starting point. A practical way to prioritise is to evaluate use cases against two dimensions: deployment complexity and operational impact.

Start here if you want the fastest path to measurable ROI:

Omnichannel customer support and fraud detection are consistently the highest-impact, fastest-to-production use cases across banking deployments. Both connect to existing systems through standard APIs, deliver measurable outcomes within weeks of go-live, and generate the audit trail and governance data you need to build confidence with leadership and regulators.

Start here if compliance is your primary pressure:

KYC automation and AML transaction monitoring address the workflows where manual effort is highest and regulatory exposure is most acute. These deployments tend to require more careful integration with existing risk frameworks, but the compliance ROI is substantial and immediately measurable.

Start here if analytics and reporting are the bottleneck:

If your leadership team is waiting too long for data and too long for answers, agentic BI is a high-speed deployment with rapid visible impact. It does not require replacing existing systems — it layers on top of data that already exists.

In any scenario, a deployment timeline of four weeks to production is achievable when the platform is pre-integrated with your core banking, CRM, and risk systems. See how assistents.ai deploys AI agents for financial services institutions.

Conclusion

AI agents in banking are no longer a future technology. They are in production, at scale, across compliance, customer operations, core banking, analytics, and fintech workflows — delivering measurable outcomes that manual and rule-based approaches cannot match.

The 25+ use cases covered in this guide represent the leading edge of where financial institutions are deploying AI agents today. The common thread across all of them is the same: AI agents work best in banking when they are built with governance as a design principle, integrated with existing systems rather than replacing them, and deployed in well-scoped use cases where outcomes are measurable and compliance requirements are explicit.

The institutions that move now — identifying their highest-friction workflows and deploying governed AI agents against them — are building operational advantages that will compound over time. The question is not whether your bank needs AI agents. The question is where you deploy them first.

Ready to see AI agents in action across your financial services workflows?

Explore assistents.ai for Financial Services →

See deployment outcomes and talk to our team →

Read the in-depth guide: AI Agents for Financial Services →

FAQs

What is the difference between an AI agent and a chatbot in banking?

A chatbot responds to questions based on pre-defined scripts or retrieval from a knowledge base. It cannot take action, execute workflows, or handle situations outside its training data. An AI agent perceives context, reasons about it, and executes multi-step tasks across connected systems — processing a loan application, filing a SAR, resolving a dispute, or updating a customer record — with minimal human intervention. In banking, this distinction is the difference between a tool that answers and a system that operates.

Are AI agents compliant with banking regulations?

Yes — when built with compliance as a design requirement rather than an afterthought. Enterprise AI agent platforms for banking include immutable audit trails on every agent action, role-based access controls, human escalation paths for regulated decisions, and governance layers that enforce policy on every workflow. Leading platforms maintain SOC 2 Type II, PCI-DSS, and GDPR compliance, with architecture designed to support AML/KYC frameworks across jurisdictions. The EU AI Act (high-risk deadline August 2026) and Colorado AI Act (June 2026) both have specific implications for financial services AI — governed agentic platforms are built to meet these requirements.

How long does it take to deploy an AI agent in banking?

For well-scoped use cases with pre-built integrations to core banking, CRM, and risk systems, production deployment is achievable in as little as four weeks. More complex multi-agent implementations — spanning compliance, operations, and analytics simultaneously — typically take eight to twelve weeks. The key variable is integration readiness: how cleanly existing systems expose data and whether governance requirements are defined upfront. Learn more about the assistents.ai implementation approach.

What ROI can banks expect from AI agents?

ROI varies by use case, but benchmarks from financial services deployments are consistently material. Compliance automation typically delivers 30–50% reduction in manual workload on AML and KYC workflows. Fraud detection agents reduce false positive rates by 60% or more in mature deployments. Customer service agents handle the majority of tier-1 queries autonomously, reducing cost-per-interaction significantly. Agentic BI eliminates reporting bottlenecks that previously consumed days of analyst time per cycle. The most reliable way to calculate institution-specific ROI is to model it against your current headcount and process volumes before committing to a deployment scope.

Can AI agents work with existing core banking systems?

Yes. Modern AI agent platforms connect to core banking systems including Temenos, FIS, Jack Henry, and Finastra through pre-built connectors, as well as to AML platforms, CRM systems, document management tools, and ERP platforms including SAP. Agents operate on top of existing infrastructure — they do not require replacing core systems. The integration layer establishes a unified data view across connected systems, which the agent then operates against. Explore the full integrations directory.

What is agentic AI in financial services?

Agentic AI in financial services refers to AI systems that can autonomously plan, reason, and execute multi-step workflows across banking, insurance, and fintech operations — without continuous human direction. Unlike earlier generations of AI that required a human to interpret outputs and decide what to do next, agentic systems take action: they create SAR filings, process loan applications, route disputes, update CRM records, and generate regulatory reports. They operate within defined governance guardrails, with human oversight at defined escalation points, making them viable in regulated financial environments.

![Agentic AI in Finance and Accounting: The Complete Guide for CFOs and Finance Leaders [2026]](/_next/image?url=https%3A%2F%2Fcdn.prod.website-files.com%2F66fb6d6d4a496c8985f663dd%2F6a29017e5cc707b20d0b88f5_pawel-czerwinski-1A_dO4TFKgM-unsplash.jpg&w=3840&q=75)