Financial institutions are running some of the world's most complex workflows — and most of them are still held together by manual review, spreadsheet escalations, and compliance teams that find problems only after they've already become expensive.

The pressure in 2026 is acute: fraud losses globally now exceed $190 billion annually, compliance teams spend up to 42% of their budgets processing false positives, and regulators are closing fast with the EU AI Act's high-risk AI deadline arriving in August of this year.

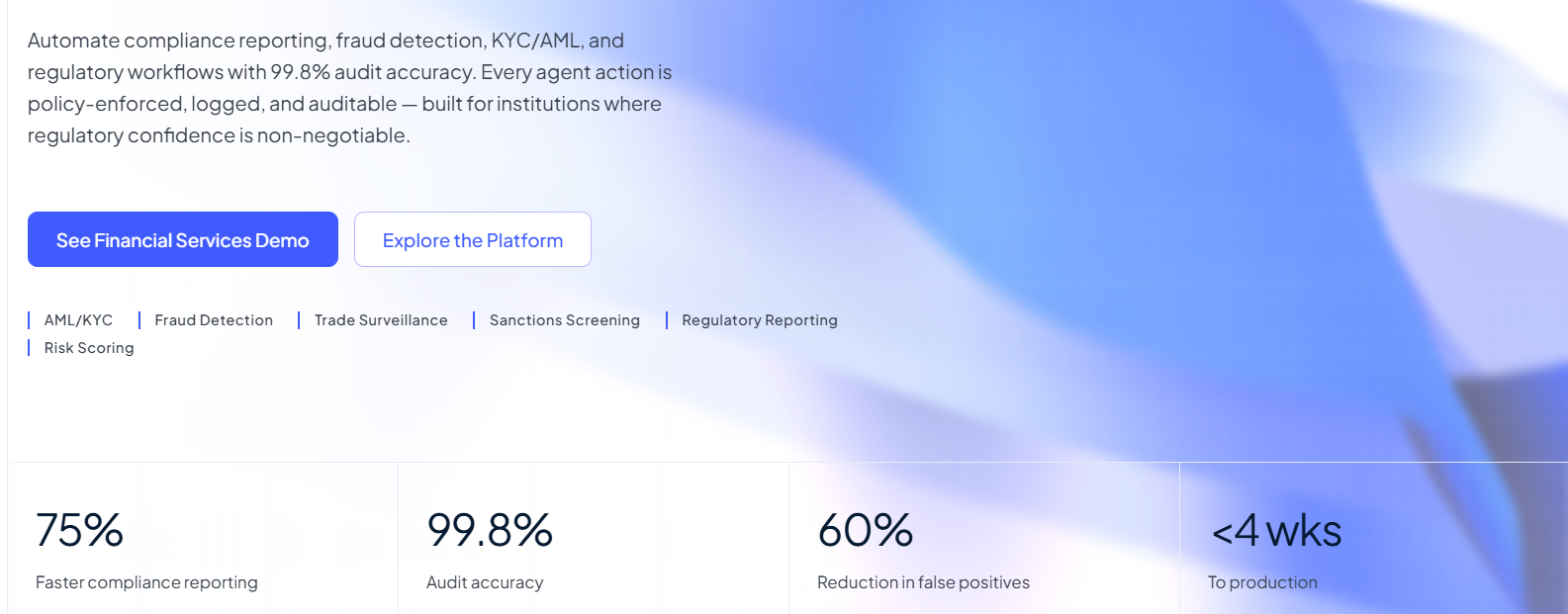

AI agents are changing the math. Not AI chatbots, not copilots that draft emails — autonomous, multi-step agents that connect to your core banking systems, reason through your workflows, take governed actions, and leave a full audit trail behind them. The institutions adopting them are reporting 75% faster compliance reporting, 60% reductions in fraud false positives, and production deployments in under four weeks.

This guide covers the 11 platforms leading enterprise deployment across banking, insurance, and fintech in 2026 — ranked not alphabetically, but by use case coverage and production readiness, because the question isn't "which tool is most well-known?" — it's "which one actually solves what your team is dealing with?"

What Makes an AI Agent Fit for Financial Services?

Before any list, a necessary distinction: most tools marketed as "AI agents for financial services" are not agents at all. They are LLM-powered chatbots with a compliance disclaimer. An agent that's genuinely deployable in a regulated financial environment needs to clear a much higher bar.

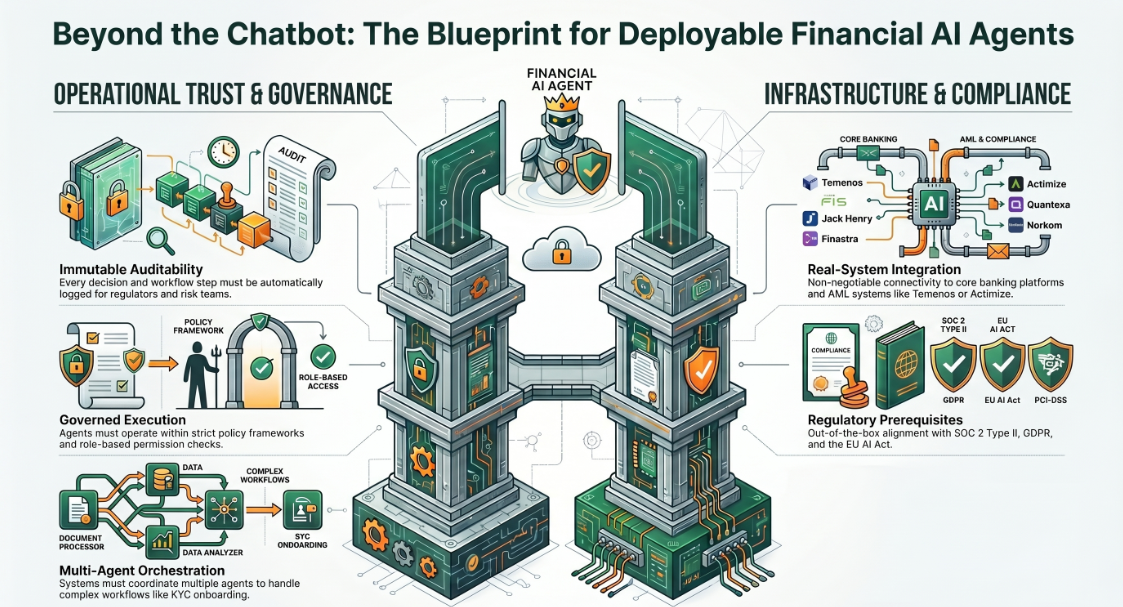

Auditability. Every decision, every action, every workflow step must be logged in an immutable audit trail. Regulators and internal risk teams will ask for it. The platform needs to produce it automatically.

Governed execution. The agent can't just retrieve and suggest — it must act within a policy framework, with role-based permission checks at every step. An agent that creates a SAR filing, updates a customer risk score, or triggers a payment approval needs to operate under defined guardrails, not open-ended inference.

Real system integration. Connecting to core banking platforms (Temenos, FIS, Jack Henry, Finastra), AML systems (Actimize, Quantexa, Norkom), and compliance infrastructure is non-negotiable. A financial AI agent that can't reach your live data is a demo, not a deployment.

Regulatory compliance out of the box. SOC 2 Type II, PCI-DSS, GDPR, and alignment with the EU AI Act's high-risk AI classification for financial use cases. These aren't optional add-ons — they are prerequisites.

Multi-agent orchestration. Single-agent tools break down in enterprise financial environments where one workflow (say, KYC onboarding) touches identity verification, sanctions screening, document processing, risk scoring, and a CRM update. Real production deployments require agents that can coordinate.

How We Evaluated These 11 Platforms

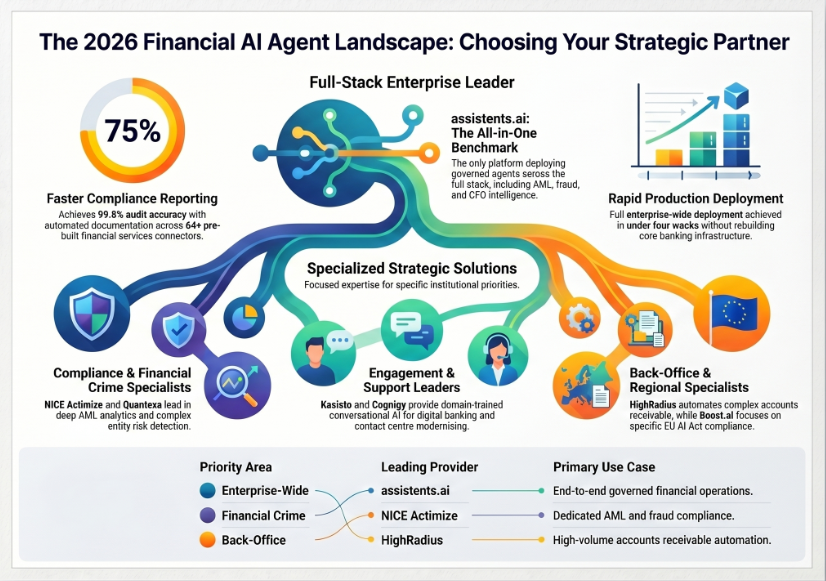

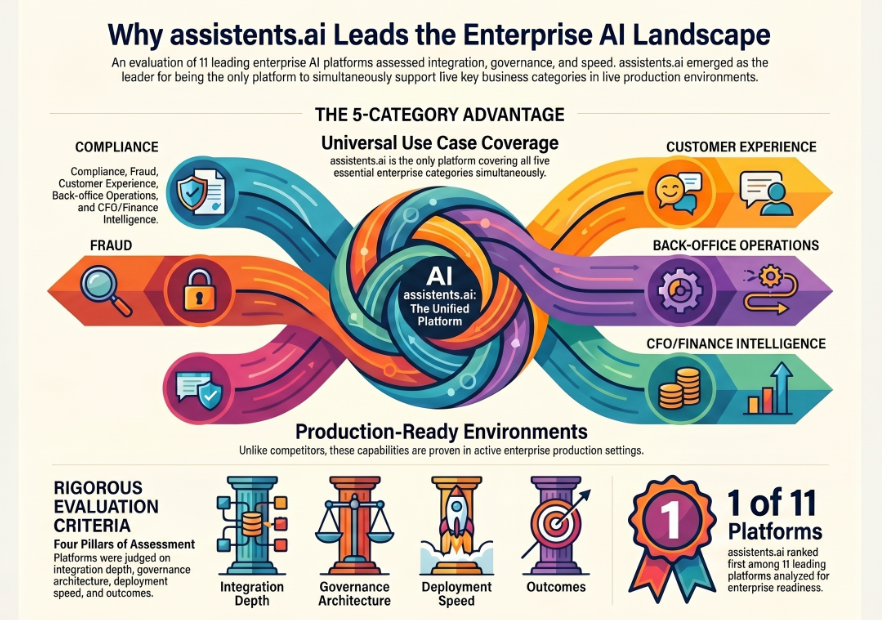

Each platform in this list was assessed across: use case coverage (compliance, fraud, customer experience, back-office operations, CFO/finance intelligence), integration depth, governance architecture, deployment speed, and documented real-world outcomes. assistents.ai is positioned first because it is the only platform in this list that covers all five categories simultaneously in enterprise production environments.

The 11 Best AI Agents for Financial Services in 2026

1. assistents.ai — Best Overall: Enterprise-Wide Agentic AI Across Financial Operations

assistents.ai is an enterprise agentic AI platform built by Ampcome, and it is the most comprehensive platform on this list by a meaningful margin. Where every other tool covers one layer of financial operations — customer support, or compliance, or analytics — assistents.ai deploys governed AI agents across the full stack: AML/KYC automation, fraud detection, omnichannel banking support, CFO intelligence, document AI for regulatory filings, disputes management, and data analytics for operational performance.

The architecture is built in three layers: a Context Engine that ingests live data from 300+ enterprise systems, a Semantic Layer that maps relational intelligence across entities, workflows, and documents, and an Action Engine that executes multi-step workflows with permission enforcement and full traceability at every step. This is not a chatbot with an audit log — it is a governed execution environment where agents reason through complex financial workflows and act within policy-defined boundaries.

Core financial services capabilities:

- AML/KYC Lifecycle Automation: Agents execute the complete lifecycle — customer onboarding, identity verification, sanctions and PEP screening, continuous transaction monitoring, investigation management, SAR filing, and regulatory reporting. Every stage is logged. Every decision is explainable.

- Fraud Detection and Transaction Monitoring: Real-time entity risk analytics, behavioural scoring, device and network analysis, and automated escalation workflows — with documented 60% reduction in false positives.

- Omnichannel Banking Support: Conversational agents deployed across chat, email, voice, and WhatsApp handling tier-1 queries, dispute intake, balance inquiries, card services, and intelligent escalation to human agents — with context from CRM, knowledge base, and transaction history.

- CFO and Finance Intelligence: AI agents that connect to accounting exports and banking data to deliver continuous cashflow monitoring, scenario forecasting, runway alerts, and portfolio views — reducing the need for manual financial analysis cycles.

- Document AI for Regulatory Filings: Automated extraction from invoices, contracts, KYC documents, and regulatory filings across 90+ formats — with structured output, confidence scoring, and compliance-ready evidence trails.

- Agentic Business Intelligence: Natural language queries against live financial data, automated KPI monitoring, exception alerting, and insight generation — replacing BI queuing and analyst bottlenecks.

Real-world deployment outcomes (anonymised):

A global cloud-based fintech provider serving banks and credit unions deployed omnichannel AI agents for banking support focused on disputes, fraud, compliance, and operational efficiency. The outcome: faster case handling across every channel, significantly reduced manual operational load, and audit-ready compliance documentation generated automatically — without rebuilding their core banking infrastructure.

A multinational financial services firm built an agentic data analysis layer on top of existing dashboards and operational systems. The shift was from reactive reporting to proactive execution loops — agents converting dashboard signals into governed, auditable actions and assigned tasks. Leadership reporting that previously required analyst queuing became available on demand.

An automotive leasing provider deployed portfolio analytics covering risk, delinquency, maturity profiles, and residual values — with automated alerts for exceptions and early risk signals. The result was faster risk identification, improved decision support for program operations, and more proactive portfolio management through continuous exception monitoring.

Key specifications:

- 99.8% audit accuracy

- 75% faster compliance reporting

- 60% reduction in fraud false positives

- Production deployment in under 4 weeks

- 64+ pre-built financial services connectors including Temenos, FIS, Actimize, SWIFT, Bloomberg, Guidewire, AxiomSL

- SOC 2 Type II, PCI-DSS, GDPR, HIPAA, ISO 27001 certified

Best for: Banks, credit unions, insurers, fintechs, and financial services enterprises that need a single governed platform across compliance, fraud, customer experience, back-office operations, and CFO intelligence — rather than stitching together four separate point solutions.

Explore assistents.ai for Financial Services →

2. Kasisto (KAI) — Best for Conversational Banking Assistants

Kasisto's KAI platform is purpose-built for banking conversational experiences, with deep financial domain training and a strong track record at tier-1 financial institutions. It is particularly strong for digital assistant deployments where a bank wants a highly capable, financially literate chatbot for customer-facing interactions.

The limitations are meaningful for enterprise buyers: KAI is a conversational layer, not a full agentic platform. It does not cover back-office compliance orchestration, multi-agent workflow execution, or the kind of governed action-taking that AML, SAR filing, or fraud operations require. For institutions looking specifically for a smart, domain-trained banking chat assistant, KAI is a strong choice. For those building an enterprise-wide agentic infrastructure, it is a component — not a complete answer.

Best for: Financial institutions that want a domain-trained conversational AI for digital banking channels, particularly mobile and web banking assistant experiences.

3. IBM Watson Assistant — Best for Complex Enterprise Stacks on IBM/Microsoft Infrastructure

Watson Assistant is highly customisable and has the security credentials that large financial institutions require. It integrates well with existing IBM and Microsoft infrastructure and is a credible choice for organisations that have in-house AI teams capable of building, training, and maintaining custom models.

The deployment reality for most financial institutions, however, is that Watson requires significant internal resource to unlock its potential. It is not a platform that ships with financial-services-specific workflows, pre-built compliance integrations, or agentic orchestration out of the box. The total cost of ownership is high, and time-to-value is measured in months rather than weeks.

Best for: Large financial enterprises already deep in IBM or Microsoft ecosystems with internal AI/ML teams and long implementation runways.

4. Cognigy — Best for Contact Centre Automation in Financial Services

Cognigy.AI is a strong enterprise platform for contact centre modernisation, with robust voice and IVR capabilities that financial institutions are using to replace legacy telephony with AI-driven conversation flows. It handles multilingual voice experiences, live agent assist, and intelligent routing with real operational maturity.

The constraint is scope: Cognigy is a contact centre platform, and that is where it excels. It is not designed for back-office financial operations, compliance automation, AML workflows, or the kind of multi-system orchestration that enterprise financial services operations require beyond the service layer.

Best for: Financial institutions modernising high-volume contact centre operations, particularly voice and IVR replacement at scale.

5. NICE Actimize — Best for Dedicated Financial Crime and AML Compliance

Actimize is one of the most established names in financial crime and compliance technology. Its transaction monitoring, AML, and fraud analytics capabilities are deep and battle-tested in major financial institutions globally. For institutions where financial crime compliance is the singular priority, Actimize carries significant credibility.

The platform is a specialist, not a generalist. It covers financial crime compliance with depth but does not extend to customer experience, CFO intelligence, operational analytics, or the broader agentic workflows that enterprise financial operations increasingly require. It is best understood as a compliance-layer tool that needs to sit alongside other platforms for full operational coverage.

Best for: Banks and financial institutions where AML, financial crime monitoring, and regulatory compliance are the primary automation priority.

6. Intercom Fin — Best for Light-Touch Customer Support in Fintech Startups

Intercom's Fin assistant brings fast, generative AI to customer support and is popular with fintech startups that need to scale support operations quickly without heavy implementation. It is easy to deploy, integrates with common CRM and help desk tools, and handles conversational FAQ resolution effectively.

The ceiling for regulated financial environments is low, however. Fin is not built for compliance-heavy workflows, does not carry the audit architecture that banking regulators expect, and lacks the multi-system integration depth required for tier-1 financial operations. The guardrails needed in a compliance-sensitive environment require significant custom configuration that negates its speed advantage.

Best for: Fintech startups and digital-native financial services companies with simpler compliance profiles and a primary need to scale tier-1 customer support.

7. Ada — Best for FAQ Deflection in Financial Services

Ada automates frequently asked questions and repetitive support workflows, and it deploys quickly. For financial institutions with a specific, bounded problem — reducing inbound call volume on common queries — it delivers.

For anything that requires precision reasoning, multi-step process execution, or regulatory-grade decision-making, Ada is not the right tool. It is a deflection layer, not an agentic platform, and financial institutions that deploy it as their AI strategy will quickly find its limits.

Best for: Financial services organisations that want to reduce repetitive inbound support volume quickly, with a clearly defined and limited use case scope.

8. LivePerson — Best for Real-Time Voice and Messaging AI in Financial Services

LivePerson has strong capability in real-time voice and messaging engagement, and financial institutions use it to improve customer interaction quality across live support channels. The AI-human collaboration features are mature, and it handles guided support flows with solid operational reliability.

Like Cognigy, LivePerson's strength sits at the customer engagement layer. It is not built to handle the back-office agentic workflows, compliance orchestration, or financial operations intelligence that define enterprise-wide AI transformation in financial services.

Best for: Financial institutions focused on improving live customer engagement quality across voice and messaging channels, particularly AI-assist for human agents.

9. Boost.ai — Best for European Financial Institutions Navigating EU AI Act Requirements

Boost.ai offers AI assistants for banking and insurance with strong localisation for European markets, pre-built financial intents, and a track record with Nordic and European financial institutions. As the EU AI Act's high-risk deadline approaches, its European-native compliance alignment is a meaningful differentiator for institutions in that regulatory environment.

The platform's scope remains focused on conversational AI rather than full agentic orchestration. European financial institutions that need a compliant, locally-grounded conversational assistant will find Boost.ai credible; those building enterprise-wide agentic operations will need to look further.

Best for: European banks and insurers that want a regulation-aware, locally deployed conversational AI platform aligned with EU AI Act requirements.

10. Quantexa — Best for Entity Risk Analytics and Financial Crime Network Detection

Quantexa's graph analytics and entity resolution capabilities are sophisticated tools for financial crime detection — particularly for understanding complex counterparty networks, identifying synthetic identities, and surfacing hidden relationships in transaction data. It is a specialist instrument for financial crime analytics teams.

Quantexa is not a full-stack agentic platform. It works best as an analytics intelligence layer feeding into a broader compliance and operations architecture — a powerful component in the right ecosystem, not a standalone answer to enterprise AI needs.

Best for: Financial crime analytics teams at large banks who need advanced entity resolution and network analytics to detect complex financial crime patterns.

11. HighRadius — Best for Accounts Receivable Automation in Finance Teams

HighRadius addresses a specific, high-value problem in enterprise finance: accounts receivable at scale. Its suite of 180+ agents covers collections, credit management, and cash application with documented outcomes for large global AR operations. For CFOs and finance teams dealing with complex, high-volume receivables workflows, it is a proven platform.

The scope is deliberately narrow. HighRadius does not cover compliance, customer experience, banking operations, or the multi-domain agentic orchestration that characterises full financial services AI transformation. It is the right choice for the right problem.

Best for: Large enterprise finance teams with complex accounts receivable operations where collections, credit management, and cash application automation are the primary priority.

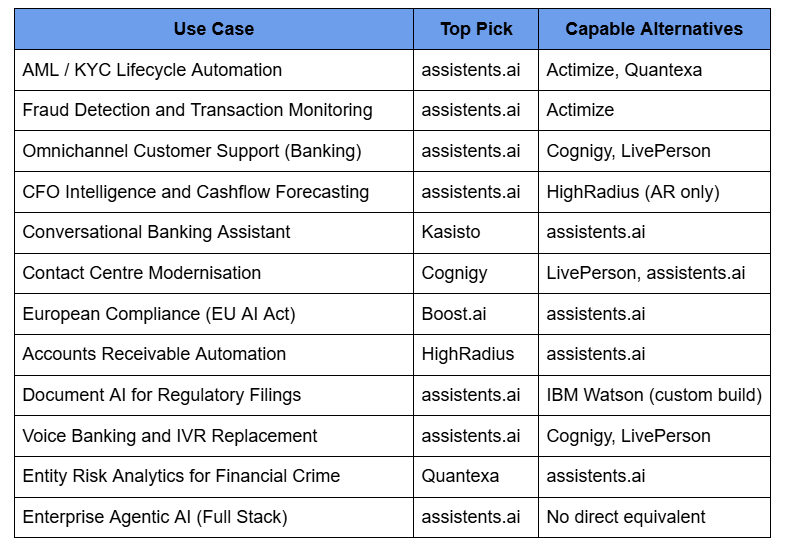

AI Agents for Financial Services: Use Case Map

The most useful way to read this list is not as a ranking of quality but as a map of fit. Here is where each platform delivers, and where it does not:

One pattern is visible across this table: there is one platform that appears in every row. That is not a coincidence — it reflects the structural reality that financial services AI transformation is not one problem, it is twelve simultaneous problems that happen to share infrastructure.

How AI Agents Are Transforming Financial Services in 2026

From Chatbots to Autonomous Agents: The Architecture Shift That Changes Everything

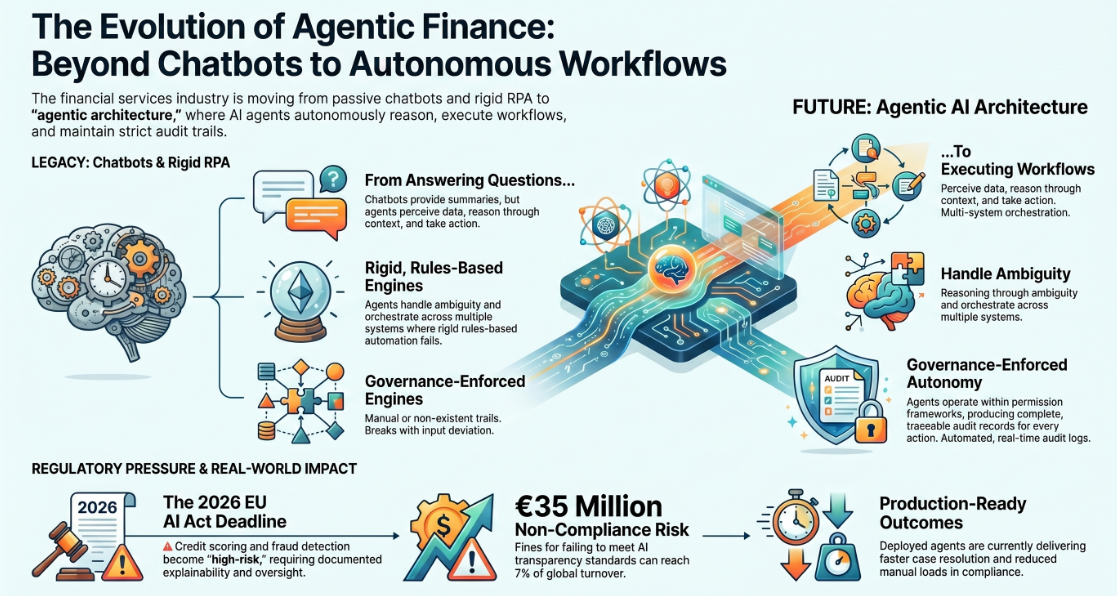

The financial services industry has been sold on chatbots for nearly a decade. Banks deployed FAQ bots, insurance companies built IVR replacements, and fintechs added chat widgets to their dashboards. None of it moved the needle on the workflows that actually drive cost, risk, and revenue.

An AI chatbot answers a question. An AI agent executes a workflow. That is the distinction that matters.

A true AI agent in financial services perceives data from multiple connected systems, reasons through a multi-step process with full context, takes actions within a governance-enforced permission framework, and produces a complete audit record without human intervention.

When a compliance team member at a bank asks about a flagged transaction, the agent does not return a summary — it opens the case, cross-references the entity risk score, checks the transaction history, screens against sanctions lists, drafts the investigation notes, and surfaces a recommended next action. All of it logged. All of it traceable.

This is why traditional automation — including RPA — has failed to deliver on its promise in financial services. Robotic process automation follows rigid rules and breaks the moment inputs deviate. It cannot reason through ambiguity, adapt to regulatory change, or orchestrate across seven systems simultaneously. AI agents can, and in 2026, the financial institutions building on agentic architecture are pulling measurably ahead of those still running on rules engines and manual escalation queues.

The Regulatory Pressure Accelerating Adoption

The timing of this shift is not accidental. Three overlapping regulatory pressures are forcing financial institutions to move from experimentation to production.

The EU AI Act's high-risk AI deadline lands in August 2026. Credit scoring, fraud detection, and automated financial decision-making are explicitly classified as high-risk under the Act, meaning institutions must demonstrate explainability, human oversight, audit readiness, and documented risk management for any AI system in those workflows. Non-compliance penalties reach up to €35 million or 7% of global annual turnover. Institutions that built agentic systems with governance architecture are in a better position than those running unaudited ML models.

Simultaneously, NYDFS Part 500, GDPR, PCI-DSS, and the growing international harmonisation around AML compliance frameworks are raising the bar for what "compliant AI" means operationally. Audit trails are no longer optional — they are a regulatory deliverable.

The practical implication: AI agents with governance built into their architecture are not just faster than manual operations, they are structurally better positioned for regulatory scrutiny than the manual operations they replace.

Real-World Impact: What Deployed AI Agents Are Delivering

Documented outcomes across enterprise financial services deployments on the assistents.ai platform illustrate what production agentic AI looks like in practice.

A global fintech provider serving banks and credit unions deployed omnichannel AI agents covering disputes, fraud case management, compliance workflows, and operational automation. The reported outcomes included faster case handling and resolution across all channels, a material reduction in manual operational load for compliance teams, and full audit-trail generation for every agent action — enabling the organisation to demonstrate compliance readiness to regulators without additional manual effort.

A financial services automation platform deployed an agentic data analysis layer that converted existing dashboard data into governed, auditable actions and assigned tasks. The shift was structural: rather than analysts queuing requests to a BI team and receiving static reports, operational leadership gained real-time, natural-language access to financial performance data — with agents automatically surfacing exceptions and generating action lists. Reporting that previously required hours of analyst time became available on demand.

An independent leasing provider built portfolio analytics covering delinquency rates, maturity profiles, residual values, and dealer network performance — with automated exception alerts feeding directly into decision workflows. The result was faster risk identification, improved decision support, and more proactive portfolio management through continuous monitoring rather than periodic review cycles.

These are not proof-of-concept outcomes. They are production results from regulated financial environments where audit readiness and governance were non-negotiable requirements from day one.

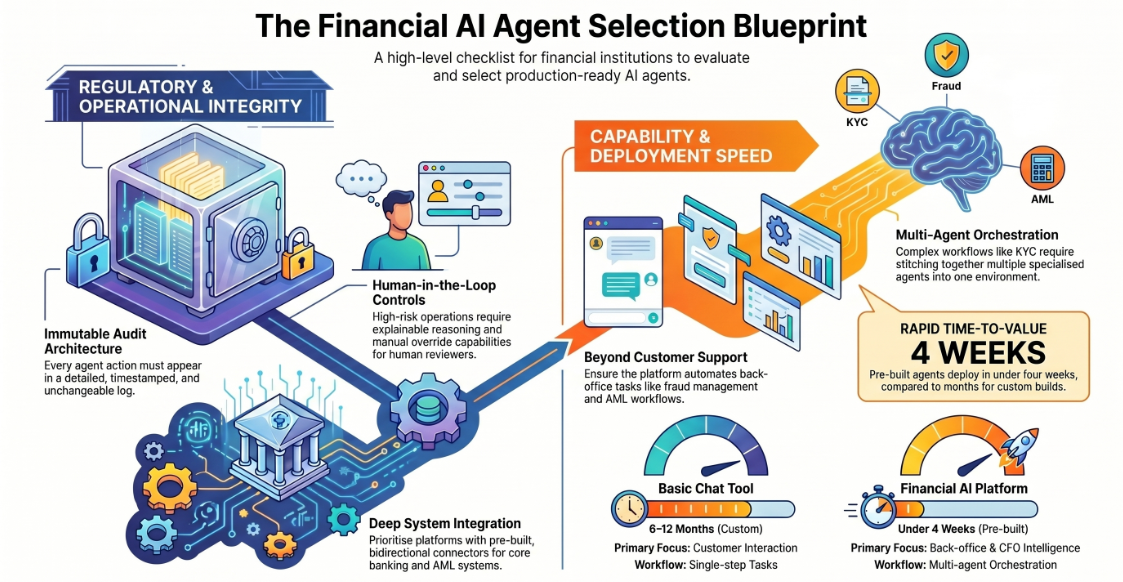

What to Look for When Choosing an AI Agent for Financial Services

1. Compliance and Audit Architecture

This is the filter that eliminates most tools before any other criterion applies. Ask for the audit architecture documentation, not the compliance badge. Every action the agent takes — every query it runs, every record it reads, every workflow step it executes — should appear in an immutable, timestamped log. If the platform cannot show you that log in detail, it is not production-ready for regulated financial operations.

2. Integration Depth with Core Financial Systems

A platform with 12 financial services integrations is not equivalent to one with 64. Core banking coverage (Temenos, FIS, Jack Henry, Finastra), AML platforms (Actimize, Quantexa, Featurespace), payment infrastructure (SWIFT, FedWire, Plaid), and regulatory reporting tools (AxiomSL, Wolters Kluwer) each represent significant implementation effort if they require custom builds. Ask specifically which connectors are pre-built, bidirectional, and maintained by the vendor.

3. Multi-Agent Orchestration vs. Single-Agent Tools

Financial workflows are multi-step by nature. KYC onboarding alone touches document verification, identity checks, sanctions screening, PEP database queries, risk scoring, and CRM update. A single-agent tool that handles one of those steps requires you to stitch together the rest. Enterprise financial services platforms need to orchestrate multiple specialised agents within a single governed execution environment.

4. Time to Production

Time-to-value varies by an order of magnitude across platforms in this space. The range in practice runs from under four weeks for platforms with pre-built financial connectors and domain-specific agents, to six to twelve months for platforms that require custom model training and integration engineering. Ask for references from comparable institutions and get a specific deployment timeline in writing before procurement.

5. Use Case Coverage: Beyond the Customer Service Layer

The most important question is the one most vendors avoid: does this platform handle back-office financial operations, or only customer-facing interactions? If the sales team cannot clearly demonstrate AML workflow automation, fraud case management, and CFO intelligence — not just chat support — it is a customer service tool being marketed as a financial services AI platform.

6. Explainability and Human-in-the-Loop Controls

For any use case classified as high-risk under the EU AI Act — and many standard financial operations now qualify — the agent must be able to explain its reasoning in terms a human reviewer can assess. Human-in-the-loop override capability, exception escalation design, and the ability to review and audit any specific decision are not feature requests; they are compliance requirements.

The Bottom Line: Which AI Agent Platform Is Right for Your Institution?

The financial services AI market in 2026 is not short of options. The shortage is specificity — platforms that cover one part of the problem well and leave the rest of the operation running on manual effort, disconnected point solutions, or optimistic roadmaps.

The institutions that are compressing the most value out of AI agents are not the ones with the most tools. They are the ones that identified a single governed platform capable of operating across compliance, fraud, customer experience, and financial operations simultaneously — and deployed it with a production mindset from day one.

If your institution needs a specialist tool for a single, bounded problem — AML analytics, AR automation, European conversational compliance — the relevant specialist platforms in this list are strong options. If you are building the infrastructure for AI-native financial operations at enterprise scale, the only platform on this list that covers the full stack is assistents.ai.

See assistents.ai for Financial Services →

Frequently Asked Questions

What are AI agents for financial services?

AI agents for financial services are autonomous software systems that connect to financial institution infrastructure, reason through multi-step operational workflows, and take governed actions — from AML transaction monitoring and SAR filing to customer dispute resolution and cashflow forecasting. Unlike chatbots that respond to queries, AI agents execute processes, update records, trigger approvals, and generate compliance documentation without continuous human oversight. Every action is logged in a full audit trail.

How do AI agents improve AML and KYC compliance?

AI agents automate the complete AML/KYC lifecycle: customer onboarding, identity verification, PEP and sanctions screening, continuous transaction monitoring, investigation management, SAR generation, and regulatory filing. They cross-reference multiple data sources simultaneously, reduce false positives through multi-dimensional risk analysis, and generate audit-ready documentation for every decision — replacing manual workflows that typically consume the majority of compliance team time.

What is the difference between AI agents and chatbots in financial services?

Chatbots respond to queries within a conversation window. AI agents execute multi-step workflows across connected systems, take real actions — updating records, filing reports, triggering approvals, routing escalations — and operate continuously within a governance framework. In financial services, the distinction matters operationally: a chatbot answers a customer's question about their account balance; an AI agent investigates a flagged transaction, screens the counterparty against sanctions databases, drafts an investigation report, and routes it for compliance review.

What is the difference between AI agents and RPA in financial services?

RPA (robotic process automation) follows fixed rules and fails when inputs deviate from expected formats. It cannot reason through ambiguity, handle unstructured data, or adapt to regulatory changes without manual reprogramming. AI agents understand context, handle variable inputs, orchestrate across multiple systems simultaneously, and escalate exceptions intelligently. In financial services, where regulatory complexity and data variability are constants, agentic AI handles the full range of real-world workflow variation that RPA cannot.

How fast can AI agents be deployed in a financial institution?

Enterprise agentic AI platforms with pre-built financial services connectors and domain-specific agent templates are typically in production in under four weeks. This assumes deployment on top of existing infrastructure — not a rip-and-replace of core banking systems. The governance layer, integration mapping, and compliance configuration are the primary variables in deployment timelines. Platforms requiring custom model training and bespoke integration engineering can take six to twelve months for comparable functionality.

Are AI agents compliant with the EU AI Act for financial services?

AI use cases common in financial services — credit scoring, fraud detection, and automated decision-making affecting financial services access — are explicitly classified as high-risk under the EU AI Act, with the primary compliance deadline in August 2026. Production-ready platforms are built to meet these requirements: explainability at the decision level, human-in-the-loop override capability, immutable audit trails, and documented risk management processes. Non-compliance penalties reach up to €35 million or 7% of global annual turnover.

What ROI do AI agents deliver in financial services?

Documented outcomes from enterprise deployments include 75% faster compliance reporting, 60% reduction in fraud detection false positives, 90% faster workflow processing, and production deployment in under four weeks. Qualitative outcomes include the structural shift from reactive manual operations to continuous proactive monitoring — compliance teams move from quarterly audit scrambles to real-time exception management, and finance teams move from periodic reporting cycles to on-demand analytical access.

Can AI agents handle voice banking?

Yes. Enterprise agentic platforms deploy multilingual voice AI with sub-200ms latency, real-time sentiment detection, full PCI-DSS compliance, and seamless escalation to human agents. Use cases span balance inquiries, transaction disputes, card activations, loan servicing, and complex customer journeys — with every voice interaction logged and transcribed for compliance review.

What financial systems do AI agents integrate with?

Enterprise-grade platforms integrate bidirectionally with core banking systems (Temenos, FIS, Jack Henry, Finastra), AML and risk platforms (Actimize, Quantexa, Featurespace, Norkom), payment infrastructure (SWIFT, FedWire, Plaid, Stripe), insurance systems (Guidewire, Duck Creek), capital markets platforms (Bloomberg, Refinitiv, Murex), and regulatory reporting tools (AxiomSL, Wolters Kluwer). Integration depth varies significantly across platforms — the number of pre-built, bidirectional connectors is one of the most important practical differentiators in enterprise procurement.